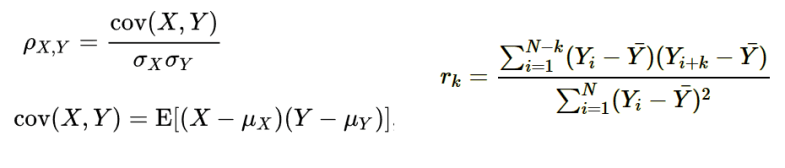

Co-variance vs Correlation

- Correlation is co-variance divided by standard deviation of both variables

- Hence it is independent of units and is always between -1 and 1, which makes comparison easier

- Formula on the right is time series specific

- It is auto correlation coefficient at lag k

- It is define as ration of auto-correlation at lag k divide by auto-correlation at lag 0

- This values are plotted on correlogram (See one for MA(2) process below)

Stationary Time Series

- No systematic change in mean (No trend)

- No systematic change in Variance

- No periodic variation (Seasonality)

If time series is not stationary we apply several transformation to make it stationary.

For example applying difference operator to random walk makes it stationary.

Random Walk

- Previous value of noise

- If first value is zero then current value is summation of all the noises so far

- X(t) = X(t-1) + Z(t)

- Z(t) = Normal (mu, sigma2)

- if X(0) = 0 then X(t) = sum(Z(k)) k form 0 to t

- Expectation[X(t)] = t*mu – – Changes with time

- Variance[X(t)] = t*sigma2 – – Changes with time

- Not a stationary process

- let Y(t) = X(t) – X(t-1) = Z(t) – – Y(t) is a stationary process

Example of Stationary Process

Moving average and Auto regressive processes described here can be stationary under conditions described here.

References

- https://onlinecourses.science.psu.edu/stat510/node/48

- https://www.coursera.org/learn/practical-time-series-analysis/home/week/2

- https://www.itl.nist.gov/div898/handbook/eda/section3/eda35c.htm

Further reading