Moving Average Processes MA(q)

- Stock price depends on announcements of last two days

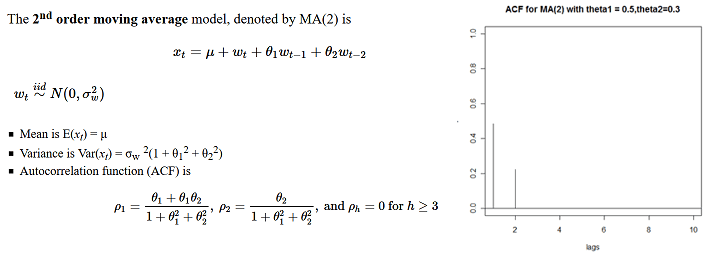

- Auto correlation function cuts off at q

Auto regressive Processes AR(p)

- Below are the plots for AR(2) process

- Depending upon the value of phi1 and phi2 ACF has alternative positive and negative values

Writing AR(p) process as MA process by substituting values of X(t-1). And yes phi is constant, we don’t need phi1, phi2 anymore.

Mean, variance and auto-correlation of AR(p) process, we have assumed Z = Norm(0, sigma2)

ACF of AR-p using Yule-Walker Equation

- It is a method of solving difference equation in recursive relation

- We first obtained auxiliary equation (also known as characteristic equation) which is polynomial and find root of that

- Using these root we get weighted geometric series and find weights using some initial condition

- We had learned in mathematics that this way of solving difference equation also related to solving differential equations

- In the course they had solved it for Fibonacci series and root had come out to be golden ratio

- For AR(p) ACF comes out to be difference equation, solving which can give us ACF for different values of lag

Reference

https://www.coursera.org/learn/practical-time-series-analysis/home/welcome

https://en.wikipedia.org/wiki/Autoregressive%E2%80%93moving-average_model